Platform Banking & Value Accrual in Fintech

On a recent trip to San Francisco, SynapseFI, a US fintech connectivity layer bridging the gap between fintechs and regulated banking infrastructure, was the subject of many conversations. The company connects regional banks to its platform and leverages their infrastructure and licenses to offer banking products like cards and FDIC-insured deposit accounts to consumer fintechs. Banking-as-a-service or platform banking has existed in other parts of the world for years, with Fidor, SolarisBank, Wirecard, Bancorp, Railsbank and ClearBank all having had varying degrees of success with the model.

Why is this topic so relevant now? The convergence toward comprehensive digital finance offerings by everyone from Revolut to WealthFront to MoneyLion is picking up pace. Plus, telecom providers and other consumer brands now have more tools than ever available to offer banking services to their massive captive customer bases, supported by the likes of Fidor (O2 Banking), Customers Bank (T-Mobile Money), Banked, the UK open banking platform opening banking up to non-financial companies, and many others.

There are clear similarities between Open Banking connectivity in Europe, where it’s required by law, and competition-driven connectivity like SynapseFI. I continue to be of the view that Open Banking in Europe was a blessing for incumbent banks, forcing them to reckon with a digital world rather than continue to bury their heads. If they fail, it won’t be because they were taken by surprise.

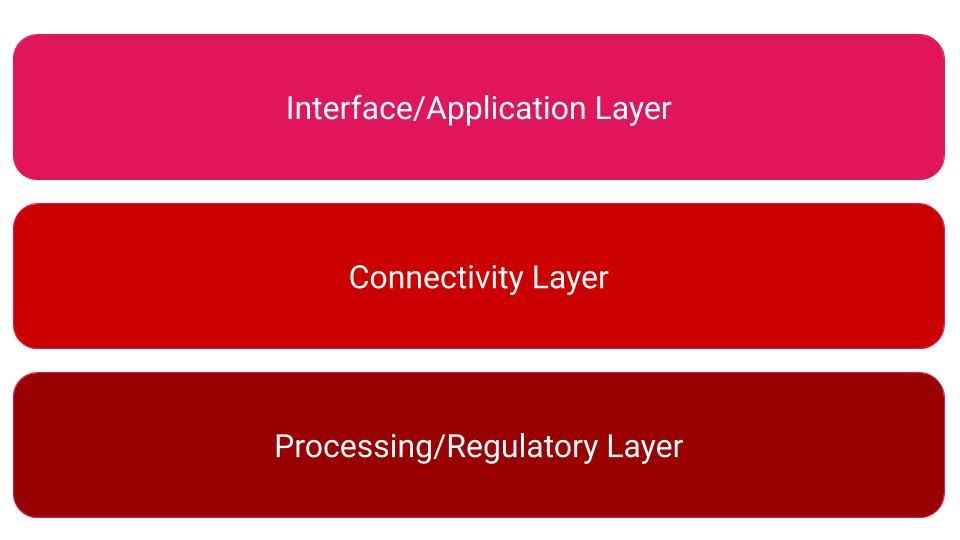

How should we think about the platform push? Financial services is organizing into three distinct layers: application/interface, integration/connectivity and processing/regulatory, with different competitive and value accrual dynamics inherent in each layer. The layer we’re focusing on here is the middle one. It’s optimized on low margins and high volumes, and it's most relevant in a rapidly evolving market.

Some see the trend of leveraging existing infrastructure as a happy extension of the “collaboration not competition” mentality people love extolling at conferences, but that’s naive. Financial services is always competitive, not collaborative. In competitive markets, businesses build niches for themselves at different points in the value chain, selling to and buying from each other in various ways. Partnerships of this type are hotly-negotiated and often short-lived stepping stones enabling one side to quickly roll out a new capability before eventually making the investment to bring the infrastructure in-house.

Monzo is a great example of this. They recently launched a savings account in partnership with mega-unicorn OakNorth in which Monzo customers can open OakNorth savings accounts from within the Monzo app. Monzo customers get one-stop banking (unbundling what?), receiving a lower interest rate than they’d get by going straight to OakNorth. Monzo gets a clip and OakNorth gets new deposits. A momentary win-win for Monzo, who isn’t in the lending business and doesn’t want deposits. Once Monzo finds a profitable use for deposits (that’s what banks do, after all!), this relationship will go away.

On a roll, Monzo is also reportedly in talks with BlackRock, Fidelity and Vanguard on a digital investment offering, modernizing and significantly undercutting the UK’s leading “discount” brokerage, Hargreaves Lansdown, which charges dotcom-era fees of £12.99 per trade plus an annual cost of as much as 45 basis points for the pleasure of owning funds on its platform. Don’t expect Monzo to build its own custody and clearing anytime soon, but FreeTrade is doing just that and reaping dramatic cost benefits over running on incumbent rails. Others will eventually follow suit.

Monzo's new product developments are exciting, as they test many hypotheses about strategy and competitive dynamics in consumer fintech, namely that even digital customers are happy paying more for the convenience of a one-stop bank and that once you're someone's main bank, it’s easy to expand the relationship into other areas of financial services.

In the US, the platform theme is similarly important. Bancorp, Cross River, CBW, Green Dot, Lincoln Savings Bank, Evolve and others support many consumer fintechs and digital banks. As they mature, successful fintechs move down the stack toward the processing/regulatory layer, cutting out costs and enhancing control and flexibility. Less than a year after their blundered savings account announcement, Robinhood is applying for a full national bank charter from the OCC. The move is a clear indication of the share trading app's continued push into banking and the economic and competitive benefits of owning the regulatory layer.

As if the Monzo and Robinhood data points weren’t enough, SoftBank just announced a $1 billion investment for 5.6% of German platform bank Wirecard, the rails previously or currently supporting fintechs including Curve, Funding Circle, Atom, Tandem, Revolut, Monese and Pockit. SoftBank’s investment comes despite multiple off-the-record conversations I’ve had about the challenges of working with Wirecard. Importantly though, that actually doesn’t matter much if they’re your fastest route to market and a stepping stone to standing up infrastructure of your own.

If after reading this, you have any lingering doubts about the significance of the connectivity layer, take a quick look at Wirecard's market cap, which as of writing sits at 16.8 billion Euros, vs. Deutsche Bank's of 16.2 billion Euros.